Collateralized Mortgage Obligation (CMO)

Collateralized Mortgage Obligation คืออะไร?

Collateralized Mortgage Obligation (CMO) หมายถึง ประเภทของหลักทรัพย์ที่มีการจำนอง ซึ่งมีกลุ่มการจำนองและขายมันเหมือนกับเป็นการลงทุน จัดโดยการถึงกำหนดและระดับความเสี่ยง CMOS ได้รับกระแสเงินสดเมื่อผู้กู้ชำระคืนการจำนองเป็นหลักประกันหลักทรัพย์เหล่านี้ ในทางกลับกัน CMOS จัดสรรเงินต้นและดอกเบี้ยให้กับนักลงทุนตามกฎและข้อตกลงที่กำหนดไว้ล่วงหน้า

ออกครั้งแรกโดย Salomon Brothers และ First Boston ในปี 1983 CMOS มีความซับซ้อนและรวมการจำนองที่แตกต่างกันไว้มากมาย ด้วยเหตุผลหลายประการ นักลงทุน มีแนวโน้มที่จะมุ่งเน้นไปที่กระแสรายได้ที่นำเสนอโดย CMOS มากกว่าสุขภาพของการจำนองเอง เป็นผลให้นักลงทุนจำนวนมากซื้อ CMOS ที่เต็มไปด้วยการจำนองซับไพรม์ จำนองอัตราดอกเบี้ยที่ปรับได้ จำนองที่ผู้กู้เป็นเจ้าของซึ่งมีรายได้ไม่ได้รับการตรวจสอบในระหว่างกระบวนการสมัคร และการจำนองที่มีความเสี่ยงอื่นๆ ที่มีความเสี่ยงสูง

การใช้ ECLS ได้รับการวิพากษ์วิจารณ์ว่าเป็นปัจจัยที่เป็นตัวกระตุ้นของวิกฤตการณ์ทางการเงินในปี 2007-2008 ราคาบ้านที่เพิ่มขึ้นทำให้การจำนองมีลักษณะเหมือนการลงทุนที่ปลอดภัยกระตุ้นให้นักลงทุนซื้อ CMOS และ MBS อื่นๆ ถึงกระนั้นสภาพตลาดและเศรษฐกิจนำไปสู่การยึดสังหาริมทรัพย์ที่เพิ่มขึ้นและความเสี่ยงในการชำระเงินที่โมเดลทางการเงินไม่สามารถคาดการณ์ได้อย่างถูกต้อง ผลกระทบของวิกฤตการณ์ทางการเงินทั่วโลกได้นำไปสู่การปรับปรุงกฎระเบียบที่ได้รับการจำนองที่เพิ่มขึ้น ในเดือนธันวาคม ปี 2016 ก.ล.ต. (SEC) และ Finra ออกกฎระเบียบใหม่ที่ช่วยลดความเสี่ยงของหลักทรัพย์เหล่านี้ โดยการกำหนดข้อกำหนดของอัตรากำไรขั้นต้นสำหรับการทำธุรกรรมหน่วยงานที่ครอบคลุม รวมถึงภาระผูกพันจำนองที่มีหลักประกัน

ทำความเข้าใจกับ Collateralized Mortgage Obligation

Secured mortgage obligations consist of several tranches or groups of mortgages organized by their risk profiles. tranche โดยทั่วไปแล้วจะมียอดเงินต้นที่แตกต่างกัน อัตราดอกเบี้ย เวลาที่ครบกำหนด และอัตราเริ่มต้น และเป็นตัวแทนของเครื่องมือทางการเงินที่ซับซ้อน ภาระผูกพันจำนองที่มีความปลอดภัยมีความอ่อนไหวต่อการเปลี่ยนแปลงของอัตราดอกเบี้ยและการเปลี่ยนแปลงของภาวะเศรษฐกิจ เช่น อัตราการยึดสังหาริมทรัพย์ อัตราการรีไฟแนนซ์ และอัตราการขายอสังหาริมทรัพย์ แต่ละ tranche มีวันครบกำหนดและขนาดที่แตกต่างกันและ ตราสารหนี้ จะออกเป็นคูปองรายเดือน คูปองจะประกอบไปด้วยการชำระเงินรายเดือนของเงินต้นและดอกเบี้ย

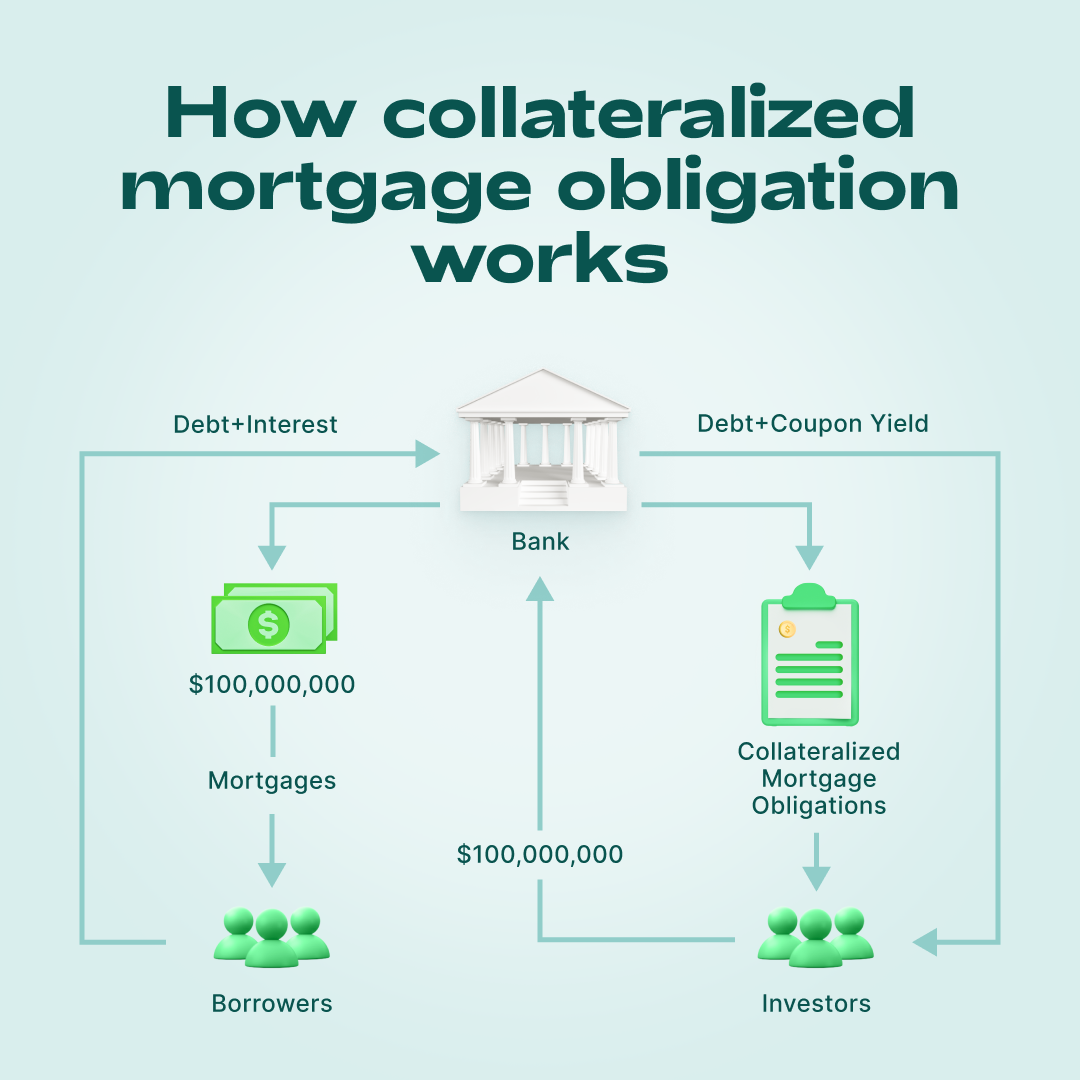

ในการยกตัวอย่าง ลองดูกลไกในภาพนี้กัน สมมติว่าธนาคารออกสินเชื่อจำนองสำหรับอพาร์ตเมนต์ในวงเงินจำนวน 100,000,000 ดอลลาร์สหรัฐ และหลังจากนั้นก็ออก CMOS ในจำนวนเดียวกันทันที กลุ่มของตราสารหนี้จะถูกยกขึ้นมาประมูล นักลงทุนได้รับรายได้ในระยะยาวที่มีความเสี่ยงต่ำจากการซื้อตราสารหนี้ ธนาคารใช้เงินที่ได้รับจากนักลงทุนเพื่อออกสินเชื่อใหม่ ส่วนหนึ่งของความสนใจในการจำนองไปที่การชำระเงินของตั๋วรายได้และส่วนที่เหลือคือกำไรของธนาคาร

CMO vs. CDO

Collateralized Debt Obligations (CDOs) ประกอบด้วยกลุ่มสินเชื่อที่รวมเข้าด้วยกันและขายเหมือนกับเป็นเครื่องมือในการลงทุน เช่นเดียวกับ CMOs อย่างไรก็ตาม ในขณะที่ CMOs มีเพียงการจำนองอย่างเดียวเท่านั้น แต่ CDOs มีเงินจากสินเชื่อต่างๆ รวมกัน เช่น สินเชื่อรถยนต์ บัตรเครดิต สินเชื่อเพื่อการพาณิชย์ และการจำนองก็ด้วยเช่นกัน ทั้ง CDOS และ CMOS รุ่งเรืองถึงขีดสุดในปี 2007 ก่อนที่จะเกิดวิกฤตการเงินโลกและมูลค่าของพวกมันก็ลดลงหลังจากนั้น ตัวอย่างเช่น ที่จุดสูงสุดในปี 2007 ตลาด CDO มีมูลค่า 1.3 ล้านล้านดอลลาร์ สำหรับการอ้างอิง ในปี 2013 มันมีมูลค่า 850 ล้านดอลลาร์

CMO vs. MBS

Mortgage-Backed Securities หรือ MBS เป็นเครื่องมือการลงทุนที่มีแพ็คเกจของการจำนองที่อยู่อาศัย องค์กรที่เสนอหลักทรัพย์ที่ได้รับการสนับสนุนจำนองซื้อเงินกู้ยืมจากธนาคารหรือสถาบันการเงิน

เมื่อผู้กู้จ่ายเงินจำนอง MBS จะได้รับเงินสด นักลงทุนใน MBS ได้รับการชำระเงินตามกำหนดเวลาที่แน่นอน รายได้ของนักลงทุนนั้นขึ้นอยู่กับเปอร์เซ็นต์ที่ตกลงกันระหว่างนักลงทุนและ MBS ที่เสนอขายหุ้นดอกเบี้ยและเงินต้นที่ทำในสินเชื่อภายใน MBS

CMO เป็นประเภทหนึ่งของ MBS สิ่งที่ทำให้ CMO แตกต่างจาก MBS แบบดั้งเดิม คือการจำนองใน CMO แบ่งออกเป็นหมวดหมู่หรือ tranche ตามความเสี่ยงและวันครบกำหนด

ความสำคัญของระดับความเสี่ยงกับ CMO

เมื่อพูดถึงภาระผูกพันจำนองที่มีหลักประกันการกำหนดระดับความเสี่ยงเป็นสิ่งสำคัญ

เนื่องจาก CMOS มักถูกจัดเป็น tranche ด้วยความเสี่ยง มันเป็นสิ่งสำคัญที่จะต้องให้ความสนใจกับพวกมัน เนื่องจาก CMO มีการเชื่อมโยงการจำนอง มีหลายสาเหตุที่ทำให้บาง tranch ถือว่ามีความเสี่ยงต่ำ เช่น การจัดอันดับเครดิตของผู้กู้ หรือจำนวนหนี้รายเดือนที่พวกเขามี

ในทางกลับกัน tranches ที่มีความเสี่ยงที่สูงขึ้นจะมีผู้กู้ที่มีเครดิตที่สูงขึ้น อัตราการยึดสังหาริมทรัพย์ที่สูงขึ้น และอัตราดอกเบี้ยที่สูงขึ้น ยิ่งมีความเสี่ยงที่ลดลงเท่าใด ก็มีโอกาสที่คุณจะได้รับเงินของคุณคืนมามากขึ้น แม้ว่าการจ่ายเงินของคุณจะต่ำกว่า ย้ำอีกครั้ง ทั้งหมดมันเกี่ยวกับสิ่งที่นักลงทุนกำลังมองหาในเครื่องมือการลงทุนโดยเฉพาะ บางครั้งนักลงทุนก็ยินดีที่จะรับความเสี่ยง หากนั่นหมายความว่าพวกเขาจะมีรายได้มากขึ้นในระยะเวลาสั้นๆ